1. a. What are the three sources of the barriers to entry that allow a

monopoly to remain the sole seller of a product?

Answer: A key resource is owned by a single firm (monopoly resource), the government gives a single firm the exclusive right to produce a good (government created monopoly), the costs of production make a single producer more efficient (natural monopoly). b.

What is the entry barrier that is the source of the monopoly power for

the following products or producers? List some competitors that keep

these products or producers from having absolute monopoly power.

1. The UK’s Royal Mail (postal service)

5. Economics, by N. Gregory Mankiw and Mark P. Taylor (your

textbook) Answer: 1. Natural monopoly. E-mail, Fax machines, telephone, private delivery such as Federal Express. 2. Monopoly resource. Other bottled water, soft drinks. 3. Government created monopoly due to a patent. Other drugs for depression, generic drugs when the patent expires. 4. Monopoly resource. Other gems such as emeralds, rubies, sapphires. 5. Government created monopoly due to copyright. Other principles of economics text books. 2.

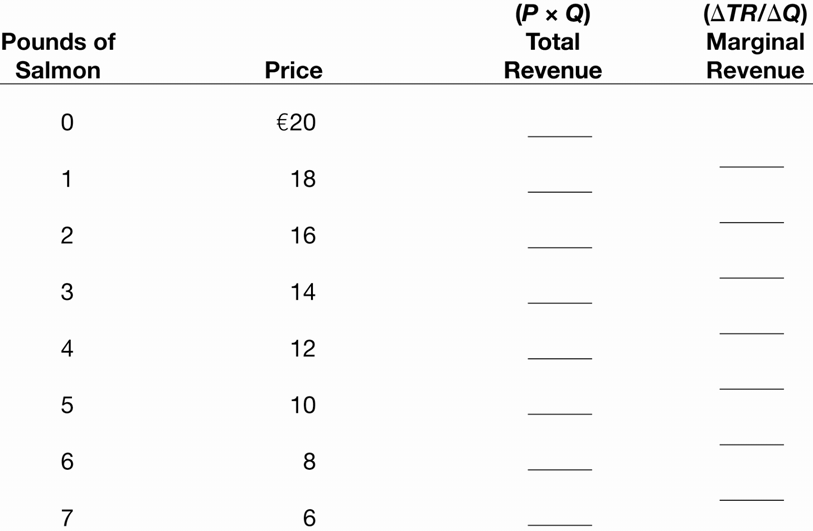

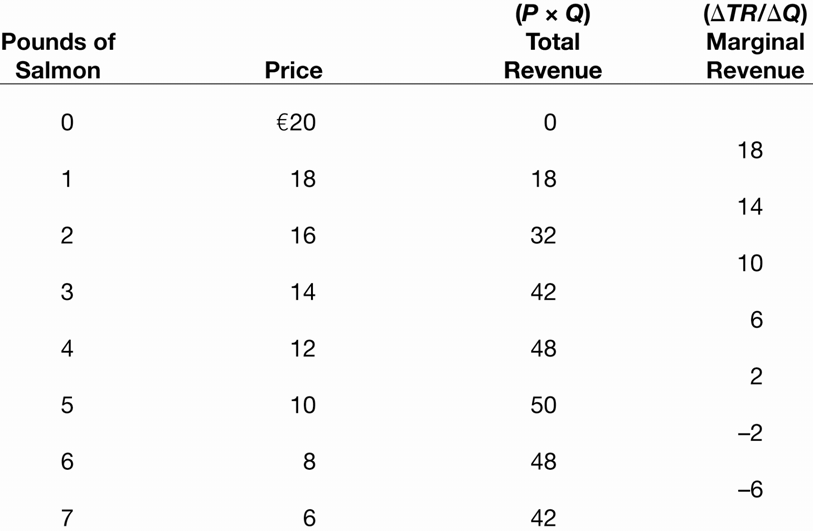

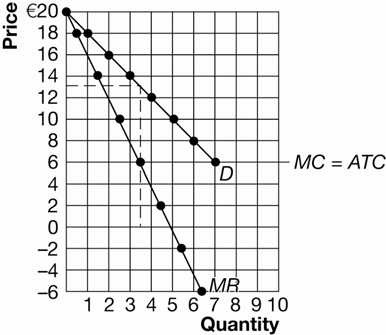

Suppose a firm has a patent on a special process to make a unique

smoked salmon. The following table provides information about the

demand facing this firm for this unique product.

Practice Questions to accompany Mankiw & Taylor: Economics

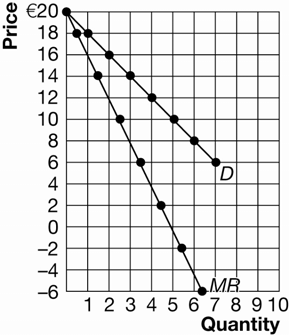

Plot the demand curve and the marginal revenue curve in Exhibit 1.

Practice Questions to accompany Mankiw & Taylor: Economics Exhibit 5

Suppose that there are no fixed costs and that the marginal cost of

production of smoked salmon is constant at €6 per kilogram. (Thus, the

average total cost is also constant at €6 per kilogram.) What is the

quantity and price chosen by the monopolist? What is the profit earned

by the monopolist? Show your solution on the graph you created in part

Answer: Q = between 3 and 4 units (say 3.5), P = between €12 and €14, (say €13). Profit = TR – TC or profit = (3.5 x €13) – (3.5 x €6) = €45.50 – €21.00 = €24.50. (Or profit = (P – ATC) x Q = (€13 – €6) x 3.5 = €24.50.) See Exhibit 6. Exhibit 6

What is the price and quantity that maximizes total surplus?

Answer: 7 units at €6 each. (The efficient solution is where the market produces all units where benefits exceed or equal costs of production which is where demand intersects MC.)

Practice Questions to accompany Mankiw & Taylor: Economics

Compare the monopoly solution and the efficient solution. That is, is

the monopolist's price too high or too low? Is the monopolist's quantity

Answer: Yes. Units from 3.5 to 7, or an additional 3.5 pounds of salmon are valued by the consumer at values in excess of the €6 per pound MC of production and these units are not produced and consumed when the price is €13. (Deadweight loss = the deadweight loss triangle = 1/2 (7 – 3.5) x (€13 – €6) = €12.25.) g.

Is there a deadweight loss in this market if the monopolist charges the

Answer: Yes. Units from 3.5 to 7, or an additional 3.5 kilograms of salmon are valued by the consumer at values in excess of the €6 per pound MC of production and these units are not produced and consumed when the price is €13. (Deadweight loss = the deadweight loss triangle = 1/2 (7 – 3.5) x (€13 – €6) = €12.25.) h.

If the monopolist is able to costlessly and perfectly price discriminate, is

the outcome efficient? Explain. What is the value of consumer surplus,

producer surplus, and total surplus? Explain.

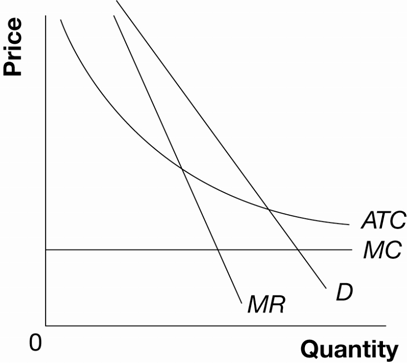

Answer: Yes, all units are produced where the value to buyers is greater than or is equal to the cost of production (7 units). Total surplus is now producer surplus and there is no consumer surplus. Total surplus and producer surplus is the area under the demand curve and above the price or 1/2(€20 – €6) x 7 = €49. Consumer surplus = €0. 3. a. What type of market is represented in Exhibit 2: perfect competition,

Answer: Natural monopoly because ATC is still declining at the quantity that could satisfy the entire market.

Practice Questions to accompany Mankiw & Taylor: Economics

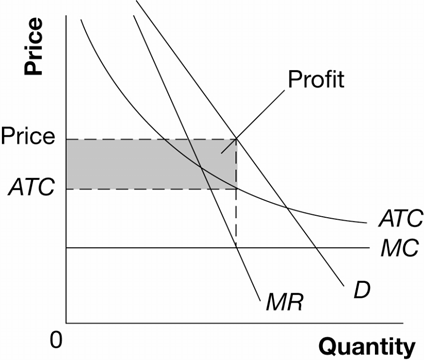

Show the profit or loss generated by this firm in Exhibit 2 assuming that

Answer: See Exhibit 7. Exhibit 7

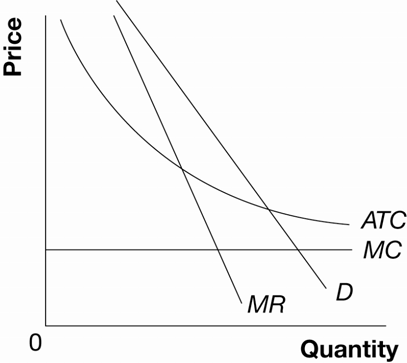

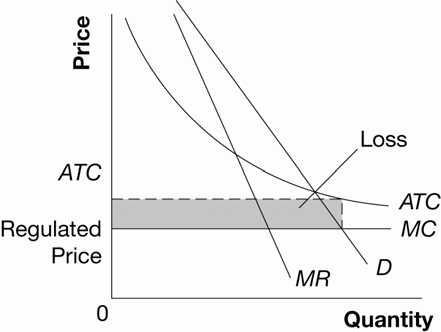

Suppose government regulators force this firm to set the price equal to

its marginal cost in order to improve efficiency in this market. In Exhibit

3 show the profit or loss generated by this firm.

Practice Questions to accompany Mankiw & Taylor: Economics Exhibit 8

In the long run, will forcing this firm to charge a price equal to its

marginal cost improve efficiency? Explain.

Answer: No. Since marginal cost must be below average total cost if average total cost is declining, this firm will generate losses if forced to charge a price equal to marginal cost. It will simply exit the market, which eliminates all surplus associated with this market.

Practice Questions to accompany Mankiw & Taylor: Economics

Dennoch herrscht auch heute noch in weiten Kreisen der Medizin die Meinung vor, in der Dermatologie nicht gäbe, oder sie sich auf ein einziges Krankheitsbild - die toxische epidermale Nekrolyse (Lyell- Deshalb ist es wichtig,auf solcheSituationen hinzuweisen, da sowohl diehäufigen wie auch seltenen spezifischendermatologischen Notfallsituationen gezielterkannt und konsequent behandelt

Creating a butterfly garden is an exiting and rewarding endeavour. It is easy to invite butterflies in to your area by gardening with their needs in mind. These beautiful insects will add bright colours and entertaining antics to your garden display. Locate the garden in a sunny area Butterflies and most butterfly attracting plants require bright sunshine. Plant nectar producing flowers Butter

Chapter 15

Chapter 15

Plot the demand curve and the marginal revenue curve in Exhibit 1.

Practice Questions to accompany Mankiw & Taylor: Economics

Plot the demand curve and the marginal revenue curve in Exhibit 1.

Practice Questions to accompany Mankiw & Taylor: Economics

Exhibit 5

Exhibit 5  Compare the monopoly solution and the efficient solution. That is, is

the monopolist's price too high or too low? Is the monopolist's quantity

Answer: Yes. Units from 3.5 to 7, or an additional 3.5 pounds of salmon are valued by the consumer at values in excess of the €6 per pound MC of production and these units are not produced and consumed when the price is €13. (Deadweight loss = the deadweight loss triangle = 1/2 (7 – 3.5) x (€13 – €6) = €12.25.) g.

Is there a deadweight loss in this market if the monopolist charges the

Answer: Yes. Units from 3.5 to 7, or an additional 3.5 kilograms of salmon are valued by the consumer at values in excess of the €6 per pound MC of production and these units are not produced and consumed when the price is €13. (Deadweight loss = the deadweight loss triangle = 1/2 (7 – 3.5) x (€13 – €6) = €12.25.) h.

If the monopolist is able to costlessly and perfectly price discriminate, is

the outcome efficient? Explain. What is the value of consumer surplus,

producer surplus, and total surplus? Explain.

Answer: Yes, all units are produced where the value to buyers is greater than or is equal to the cost of production (7 units). Total surplus is now producer surplus and there is no consumer surplus. Total surplus and producer surplus is the area under the demand curve and above the price or 1/2(€20 – €6) x 7 = €49. Consumer surplus = €0. 3. a. What type of market is represented in Exhibit 2: perfect competition,

Answer: Natural monopoly because ATC is still declining at the quantity that could satisfy the entire market.

Practice Questions to accompany Mankiw & Taylor: Economics

Compare the monopoly solution and the efficient solution. That is, is

the monopolist's price too high or too low? Is the monopolist's quantity

Answer: Yes. Units from 3.5 to 7, or an additional 3.5 pounds of salmon are valued by the consumer at values in excess of the €6 per pound MC of production and these units are not produced and consumed when the price is €13. (Deadweight loss = the deadweight loss triangle = 1/2 (7 – 3.5) x (€13 – €6) = €12.25.) g.

Is there a deadweight loss in this market if the monopolist charges the

Answer: Yes. Units from 3.5 to 7, or an additional 3.5 kilograms of salmon are valued by the consumer at values in excess of the €6 per pound MC of production and these units are not produced and consumed when the price is €13. (Deadweight loss = the deadweight loss triangle = 1/2 (7 – 3.5) x (€13 – €6) = €12.25.) h.

If the monopolist is able to costlessly and perfectly price discriminate, is

the outcome efficient? Explain. What is the value of consumer surplus,

producer surplus, and total surplus? Explain.

Answer: Yes, all units are produced where the value to buyers is greater than or is equal to the cost of production (7 units). Total surplus is now producer surplus and there is no consumer surplus. Total surplus and producer surplus is the area under the demand curve and above the price or 1/2(€20 – €6) x 7 = €49. Consumer surplus = €0. 3. a. What type of market is represented in Exhibit 2: perfect competition,

Answer: Natural monopoly because ATC is still declining at the quantity that could satisfy the entire market.

Practice Questions to accompany Mankiw & Taylor: Economics

Show the profit or loss generated by this firm in Exhibit 2 assuming that

Show the profit or loss generated by this firm in Exhibit 2 assuming that

Exhibit 8

Exhibit 8